Telecom, VoIP, and SMS Providers: A United Mission in the CPaaS Era – Why Telecom Revenues Need a New Growth Engine

The global telecom industry is under pressure. Mobile Network Operators (MNOs) face declining revenues from traditional services such as voice calls, SMS, and data. At the same time, they must continue investing heavily in 4G and 5G infrastructure. As a result, margins are shrinking across many regions.

However, this challenge also creates an opportunity.

CPaaS (Communications Platform as a Service), A2P messaging, and VoIP monetization now offer telecoms a practical path to sustainable growth. When operators combine network strength with managed communication services, they unlock new revenue streams without heavy upfront investments.

This article explains how telecoms, VoIP providers, and SMS platforms can align their mission and grow together in 2025 and beyond.

Why SMS Is Still Misunderstood and Undervalued

SMS often suffers from an outdated reputation.

Many operators view it as a declining channel, replaced by OTT messaging apps such as WhatsApp, Viber, and Messenger.

This view only tells part of the story.

To understand the real situation, we must separate two very different types of SMS traffic:

- P2P (Peer-to-Peer) messaging

- A2P (Application-to-Person) messaging

Confusing these two categories leads to incorrect conclusions.

P2P vs A2P SMS: The Critical Difference

The Decline of P2P Messaging

P2P messaging involves communication between individuals.

In this area, SMS traffic has declined. Users now prefer internet-based apps for personal conversations. This shift explains why traditional SMS volumes appear to be falling.

However, P2P represents only part of the total SMS ecosystem.

The Growth of A2P Messaging

A2P messaging tells a very different story.

Businesses increasingly rely on SMS to reach customers. Banks, airlines, e-commerce platforms, delivery services, and even OTT players send messages every day. These messages include:

- One-time passwords (OTP)

- Transaction alerts

- Delivery notifications

- Marketing campaigns

- Customer service updates

As a result, A2P traffic continues to grow year after year.

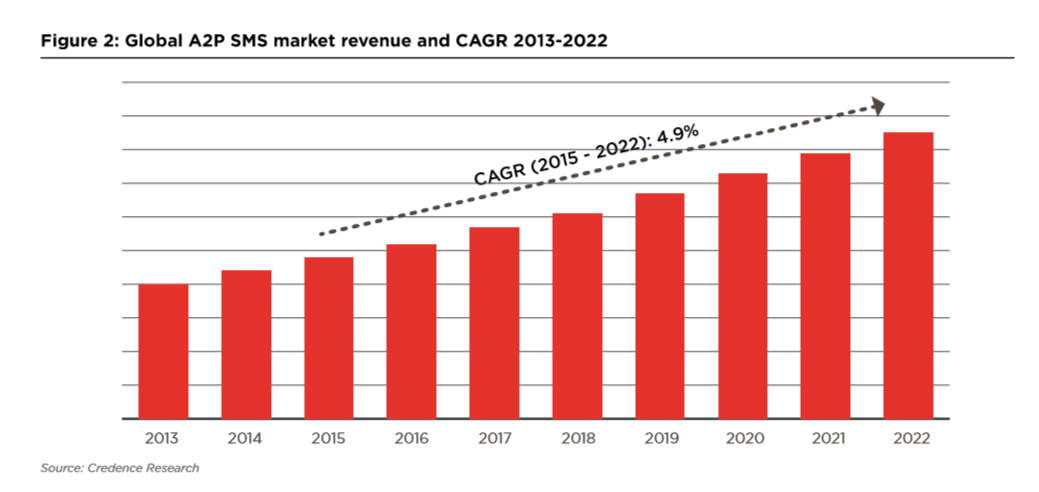

A2P Messaging: A Proven Growth Market

Industry research confirms this upward trend.

- A2P messages grew from 1.67 trillion in 2017

- Volumes reached 2.8 trillion by 2022

- Market value increased from $12 billion to $26.6 billion

- CAGR exceeded 17%

Importantly, this growth continues into the second half of the decade. Businesses prefer SMS because it delivers high open rates, instant delivery, and universal reach.

Therefore, A2P messaging remains one of the most reliable revenue sources in the CPaaS ecosystem.

OTT Players: Competitors and Contributors at the Same Time

OTT applications often receive the blame for lost telecom revenue.

Indeed, platforms such as WhatsApp, Facebook, and Skype reduced traditional voice and P2P SMS usage.

However, the same companies also generate massive A2P traffic.

They rely on SMS for:

- Account verification

- Security alerts

- Service notifications

- User authentication

As a result, OTT platforms contribute directly to A2P growth. Telecom operators still own the delivery infrastructure. The challenge lies in monetizing it correctly.

The Revenue Pressure Facing Mobile Network Operators

Market Saturation and Falling Margins

In many regions, telecom markets have reached saturation.

Subscriber growth has slowed. Price competition has intensified. Consequently, revenues continue to decline.

According to industry analysts, mobile revenues in Europe alone dropped by nearly 2% year-on-year in several periods. Similar patterns appear in North America and parts of Asia-Pacific.

The Impact of OTT Revenue Leakage

OTT services capture customer attention and service revenues.

Meanwhile, MNOs still provide the network capacity required to deliver those services.

Research estimates show:

- $14 billion lost annually to OTT voice and messaging

- Over $40 billion in SMS revenue displaced globally

This imbalance places telecom operators in a difficult position.

The Capex Challenge: Investing More, Earning Less

Since 2010, mobile operators have invested almost $1 trillion in infrastructure.

These investments include:

- Spectrum acquisition

- 4G and 5G rollouts

- Core network upgrades

- Backhaul and capacity expansion

While capex remains high, revenue growth does not keep pace. As a result, free cash flow margins continue to shrink.

Operators need new revenue models that do not require massive upfront investment.

Why A2P Messaging Fits the CPaaS Model Perfectly

A2P messaging aligns naturally with CPaaS principles.

Instead of selling raw connectivity, operators can offer communication capabilities as a service. CPaaS platforms allow businesses to integrate messaging, voice, and verification directly into their applications.

For MNOs, this model delivers several advantages:

Why A2P Messaging Fits the CPaaS Model Perfectly

A2P messaging aligns naturally with CPaaS principles.

Instead of selling raw connectivity, operators can offer communication capabilities as a service. CPaaS platforms allow businesses to integrate messaging, voice, and verification directly into their applications.

For MNOs, this model delivers several advantages:

- Faster time-to-market

- Predictable revenue streams

- Lower operational complexity

- Reduced capex exposure

Revenue Potential from A2P Monetization

The average A2P message price ranges between $0.03 and $0.04.

Even modest traffic volumes can generate meaningful revenue.

For example:

- An operator with 10 million subscribers

- Effective A2P monetization

- Proper routing and fraud prevention

Can generate $450,000 to $500,000 in annual incremental revenue.

In some markets, results exceed these estimates.

The Hidden Threat: Fraud and Grey Routes

Despite its potential, A2P messaging faces serious challenges.

Grey routes allow messages to bypass official billing channels. As a result, operators lose revenue. Industry reports estimate that up to 66% of A2P traffic may travel through grey routes in some regions.

Additionally, legacy protocols such as SS7 expose networks to security vulnerabilities.

Without proper tools, individual operators struggle to detect and block fraud in real time.

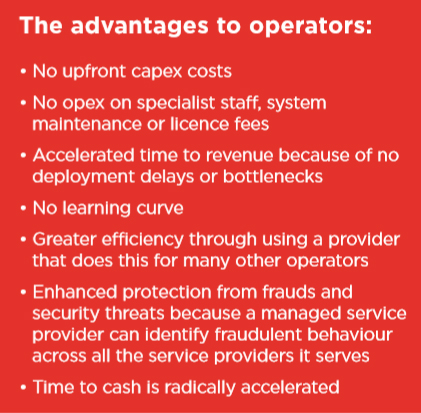

Why Managed Services Remove Barriers to Growth

A managed A2P service solves these problems efficiently.

Instead of building internal systems, operators partner with specialized providers. These partners handle:

- Traffic monitoring

- Fraud detection

- Grey route blocking

- Revenue settlement

- Market intelligence

As a result, operators avoid heavy capex and reduce operational risk.

Revenue-as-a-Service: A Smarter Monetization Model

This approach leads to a powerful concept: Revenue-as-a-Service (RaaS).

Under this model:

- The service provider manages complexity

- The operator receives revenue share

- No upfront investment is required

- Time-to-cash accelerates

Therefore, operators gain predictable income while focusing on core network performance.

A2P Messaging as a Long-Term Revenue Pillar

Market forecasts confirm the long-term value of A2P messaging.

Enterprise A2P SMS continues to expand as businesses adopt mobile-first strategies. Use cases now span retail, banking, healthcare, logistics, media, and government services.

As customer expectations rise, reliable messaging becomes essential. SMS remains the most universal channel available.

Conclusion: A Shared Future for Telecoms, VoIP, and CPaaS

Telecoms, VoIP providers, and CPaaS platforms no longer compete in isolation.

They share the same mission: delivering reliable, scalable communication services while unlocking new revenue.

A2P messaging, VoIP APIs, and managed CPaaS solutions provide the foundation for this future. By embracing these models, operators can transform declining legacy services into sustainable growth engines.

In 2025 and beyond, success will belong to those who shift from connectivity providers to communication enablers.

How 2026 Will Transform Wireless Connectivity Forever

The telecom landscape is evolving faster than ever. From AI-native networks to satellite-cellular convergence, 2026 marks a turning point where…

CPaaS 2025: Top Trends, Innovations, and What’s Next

In an era where digital-first communication is no longer optional but essential, Communications Platform as a Service (CPaaS) has become…

Why Human-First Communication Will Define the Next Decade of Business

In an age of automation, AI, and hyper-connectivity, businesses are realizing something vital: customers crave authenticity. The companies that thrive…